Worldwide gains in natural gas demand are expected to be marginal for the rest of the year, pushing down LNG spot prices and global gas benchmarks through the later half of 2024, according to the International Energy Agency (IEA).

In the IEA’s latest gas market report, researchers noted that the liquefied natural gas market would likely be capped for the rest of the year, as global export capacity is expected to expand a comparatively small 3%, or about 530 Bcf.

Meanwhile, on the demand side, falling European consumption is expected to offset growth rates in Africa, the Middle East and North America. Overall, global gas demand growth could fall to a rate below 2% in the second half of the year.

[In the Eye of the Storm: North American LNG project developers continue to grapple with the Biden administration's pause on non-FTA permits. Has the pause given impetus to other projects? How are Mexico LNG projects advancing? Tune in to hear from LNG industry analyst Sergio Chapa in the latest episode of NGI's Hub & Flow.]

“In part, the easing reflects the gradual recovery in demand, which was already underway in the second half of 2023,” IEA researchers wrote. “For the full year of 2024, global gas demand is forecast to grow by 2.5%...”

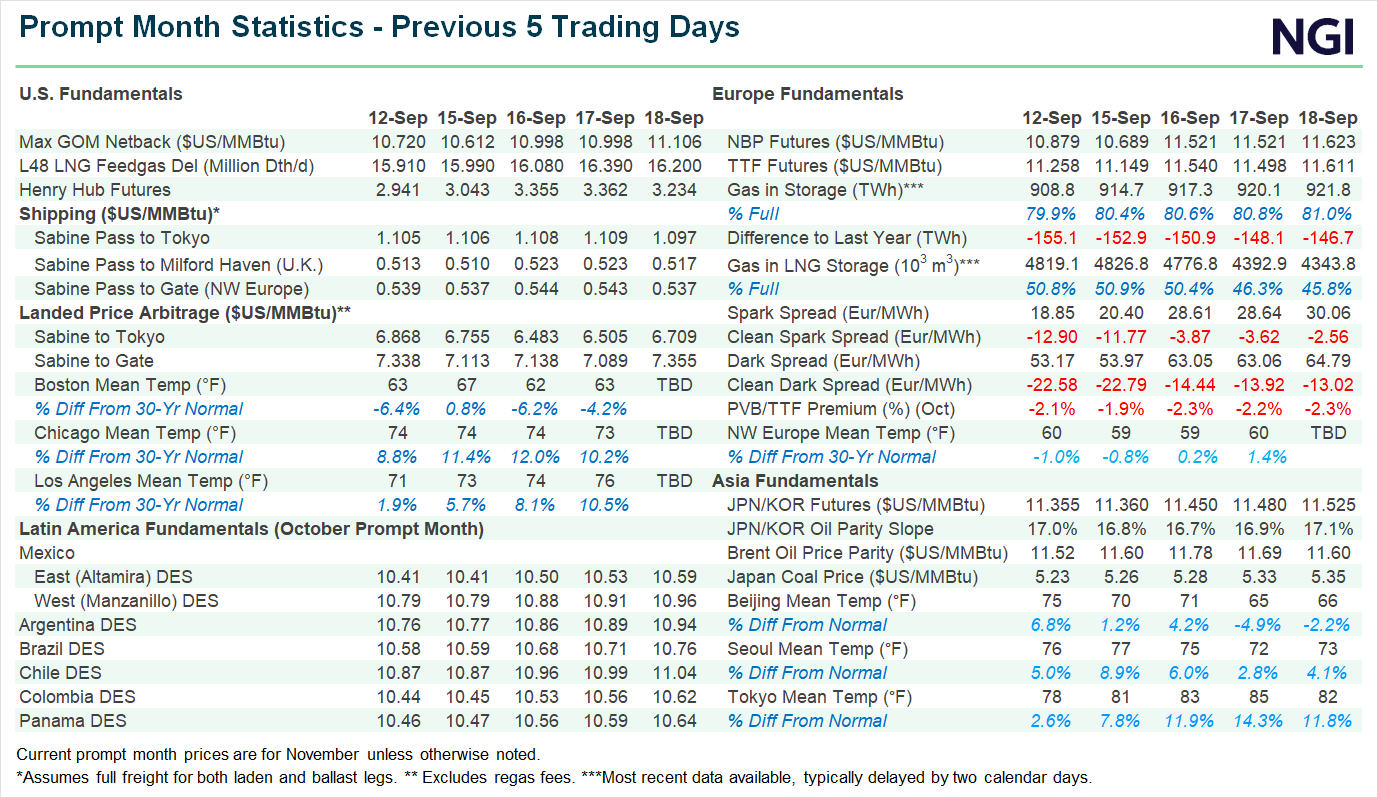

Prices And Production

Along with LNG volumes, prices are also expected to take a dip in the remaining six months of the year. IEA researchers estimated the Dutch Title Transfer Facility could average 20% below prices from the same period last year, floating around $10.50/MMBtu. Asian spot LNG prices are expected to average about $1 above European prices for most of the year.

In the United States, Henry Hub prices are forecast to stay relatively flat compared to last year, averaging $2.40 for all of 2024. The national benchmark hub for the balance of summer averaged $2.104 Thursday, according to NGI’s Forward Fixed Price data. Winter 2024/2025 prices averaged $3.161.

While U.S. prices could see little change, IEA forecast gas production is heading toward “an inflection point” in the next six months. Production volumes have trended downward in most of the gas heavy production basins in the United States this year, but could recover starting this month.

“Domestic demand growth – although modest – and LNG project start-ups in the second half of 2024 are expected to support the transition to a more dynamic market environment,” researchers said.

However, overall production is expected to be down 1% compared with the second half of 2023, leaving overall levels relatively flat year/year.

Looking For A Home

With European gas demand expected to remain flat at around 20% of the continent’s 2021 consumption levels, U.S. LNG producers would likely push more cargoes to other outlets. Europe, which has received most of its LNG from the United States since 2022, could see a 10% year/year reduction in imports by the end of the year, according to the IEA.

An outage at Freeport LNG Development LP’s terminal in Texas after former Hurricane Beryl passed through the state briefly weighed on prices, but has now mostly passed unnoticed thanks to high storage in Europe. Analysts with trading firm Energi Danmark said in a recent note that the European market is taking the situation “very calmly” compared to the volatility of two years ago.

“The supply situation in Europe is currently so good that a short-term market shake-up like this is not enough to lead to significant price spikes – neither on the daily market, nor on the nearest futures contracts,” analysts wrote.

Meanwhile, lower global prices could help spur double-digit growth in emerging Asian economies markets like Bangladesh, Pakistan, Singapore and Thailand.

Overall, “emerging Asian gas markets could grow by around 17%” year/year, adding more than 282 Bcf in LNG demand to the global market, according to IEA.

A majority of the added gas demand created by the heat waves that have struck Southeast Asia this summer have been met by the Middle East, researchers noted, but more U.S. cargoes have also headed to emerging Asian countries than last year.

Wood Mackenzie noted earlier in the week that feed gas flows to Sempra Infrastructure’s Cameron LNG have ticked down since Monday (July 15), helping contribute to an overall drop in LNG draw. Cameron LNG is on track to export 0.63 million metric tons (mmt) by July 21, which is about 0.38 mmt below the same period last year, according to Kpler data.

Almost all of the cargoes from Cameron LNG this month are headed to Asia.

Japanese power generators, some of the largest Asian customers of U.S. LNG, crossed the mid-July mark with above average LNG in storage, according to energy ministry data cited by Bloomberg.

Headed into the second half of the year, IEA estimated Japanese and South Korean power demand and gas consumption would decline. Japanese and Korean natural gas demand could drop 1% and 2% year/year respectively, thanks to surging nuclear and renewable generation.

{kind=link}