Against a backdrop of strong production, stout supplies in storage and a demand-thwarting hurricane, natural gas forward prices struggled for direction and ultimately gave up ground.

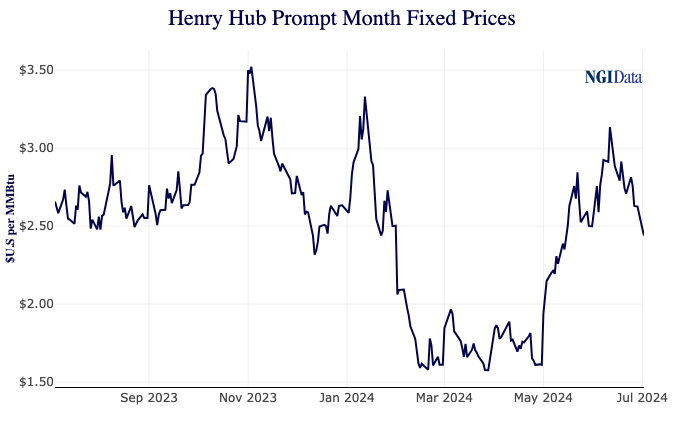

Despite intensifying heat early in July and forecasts for more in the weeks ahead, front month fixed prices at benchmark Henry Hub slipped 10.8 cents for the July 2-July 10 period, declining to $2.332/MMBtu at the close of that span, NGI’s Forward Look data show.

“People are stepping back, taking a big macro view of things and seeing a lot of moving parts, some bullish and some not so much, and that creates uncertainty,” U.S. Global Investors head trader Mike Matousek, based in Texas, told NGI. “When people are uncertain, they tend to go into wait-and-see mode.”

Fixed prices fell week/week across most regions. Chicago Citygate lost 10.6 cents to $1.871, while SoCal Citygate shed 65.5 cents to $3.125. Houston Ship Channel fell 9.3 cents to $2.000.

Waha proved a rare exception. The West Texas benchmark, which had recently traded in negative territory amid a supply glut caused by maintenance events, rebounded 77.0 cents to 76.8 cents.

Wood Mackenzie estimated on Wednesday – the final day of the latest Forward Look period – that the seven-day Lower 48 production average was 101.2 Bcf/d. That far exceeded spring lows in the mid-90s Bcf/d and was within striking distance of the summer’s peak of slightly above 102 Bcf/d.

At the same time, underground inventories remained plump. The latest storage print from the U.S. Energy Information Administration (EIA) on Thursday showed that as of July 5, supplies were 19% above the five-year average.

LNG demand, meanwhile, also was subdued during the latest Forward Look period, hovering below 12 Bcf/d – more than 1 Bcf/d from recent highs. This came in part to lingering effects from planned maintenance events, as well as former Hurricane Beryl, which made landfall in Texas at the start of this week. It caused widespread power outages and forced pauses at liquefied natural gas facilities, including Freeport LNG Development LP.

“Shoot, when a hurricane comes through, it creates the potential to mess up everything,” including energy demand, Matousek said.

He said Beryl reminded forward-looking traders of the demand-destruction capabilities of severe storms. At the same time, Matousek noted that AccuWeather and other forecasters have projected the current hurricane season could prove among the most active on record.

AccuWeather estimated the total economic loss in the United States from Beryl between $28 billion and $32 billion. While the heaviest impacts were concentrated in Texas, knock-on effects on supply chains and travel stretch the scars imposed by Beryl nationally, the firm said.

AccuWeather “continues to warn of a supercharged Atlantic hurricane season that will be bustling with activity later this summer and into autumn,” meteorologist Brian Lada said this week.

Futures Stumble

Aside from a relief rally on Monday, prompt month natural gas futures struggled throughout the first two weeks of July. On Thursday, the August contract lost 6.1 cents to settle at $2.268.

This followed a bearish storage report relative to expectations. EIA printed a build of 65 Bcf that far exceeded the medians of major polls that coalesced around the mid-50s. NGI modeled a 55 Bcf build.

The result for the July 5 period also was stout relative to the year earlier and five-year average builds, which were each 57 Bcf.

Storage “remains at robust levels,” Rystad Energy analyst Wei Xiong. “Our balances indicate healthy storage levels this winter, which will keep our Henry Hub forecast lower.”

The increase for last week boosted inventories to 3,199 Bcf, putting stocks 504 Bcf above the five-year average.

NatGasWeather said exceptional cooling demand lies ahead and could help to reduce the storage surplus relative to the five-year average. Its forecast called for intense heat across much of the country this weekend, followed by a brief reprieve. More widespread lofty temperatures are then expected through late July “for a return to very strong” national gas consumption.

“The net result of recent and coming weather patterns is for surpluses to be gradually reduced towards 400 Bcf in early August,” NatGasWeather said. “But again, while surpluses are being reduced, the pace isn’t quick enough for many and a big reason natural gas prices have plunged recently.”

Preliminary injection estimates for the week ending July 12 submitted to Reuters ranged from 18 Bcf to 55 Bcf, with an average increase of 38 Bcf. That compares with a five-year average build of 49 Bcf.

“Very low injections for the rest of July may provide near-to-medium term support for gas prices, but the long-term picture is overshadowed by robust supply,” said EBW Analytics Group’s Eli Rubin, senior analyst.